Asset Allocation

Context and asset classes

The FRR was entrusted by the legislator with the mission of “managing the funds allocated to it, in order to build up reserves to help ensure the sustainability of eligible pension schemes”. In this context, the FRR has implemented an asset allocation strategy aimed at optimising the risk-return ratio of its portfolio, in compliance with regulatory constraints and the horizon of its commitments.

Pursuant to Article L. 135-8 of the Social Security Code, the FRR’s investment horizon is now a short horizon, with €2.1 billion paid to CADES each year in accordance with the legislator’s commitments.

Objectives and Constraints

Generate performance

long-term performance while limiting the negative effects of short-term market downturns

Meet its commitments

Be able to make its annual payments of €2.1 billion to CADES. The Fund’s proper operation must be preserved.

Risk diversification

Under its prudential framework, the FRR must spread its investments in a diversified manner.

Portfolio structure

1.

Adherence to the FRR s primary objective (to honour its commitments to CADES) justifies a high level of coverage for these liabilities, achieved through hedging assets that are closely correlated with them and consist of high-quality euro-denominated corporate bonds, money market instruments and French government bonds.

2.

Intermediate-yield assets offer higher returns than hedging assets but are less risky than equities. This type of asset is well suited to the FRR s risk profile. This category comprises high-yield bonds, such as high-yield corporate bonds and emerging-market bonds, as well as equities hedged with options to reduce their risk.

3.

Unhedged equities are the asset class offering the best prospects for returns (and therefore significant value creation), albeit at the cost of a significant risk of short-term loss. A fundamental assumption in strategic asset allocation is that this risk decreases as the investment horizon lengthens. The performance of equities in developed and emerging markets depends in particular on trends in global growth and corporate profitability.

Unlisted assets are also included in the portfolio but are not directly modelled in the strategic allocation analysis. These include, for example, private debt, private equity and infrastructure. Unlisted assets offer low liquidity, which is offset by higher returns compared with their listed equivalents. They therefore present a very attractive profile for a long-term investor such as the FRR.

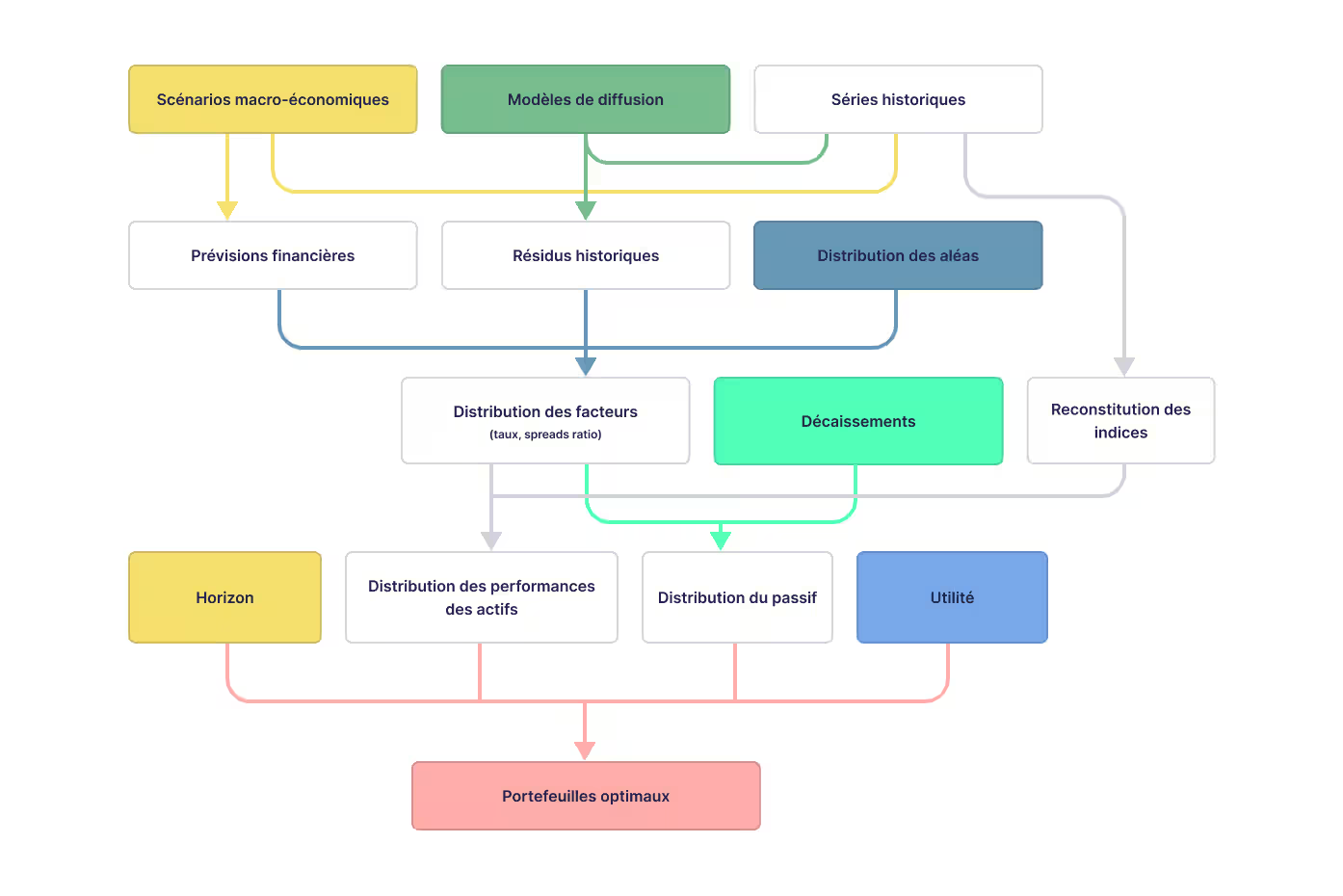

Asset allocation optimisation process

The FRR relies on an optimisation process to determine the strategic allocation that offers the best risk-return ratio for the portfolio. This process is based on liability modelling (the FRR’s commitments), the definition of return and risk assumptions for each asset class, then constrained optimisation.

The strategic allocation is proposed by the Executive Board and approved by the Supervisory Board. It is reviewed periodically in light of market developments and FRR commitments.